Download white papers

Sharpen your financial strategy with expert insights

Sharpen your financial strategy with expert insights

Advanced Financial Planning and Value Based Management

A white paper that outlines proper Advanced Financial Planning and Value Based Management through a practical example.

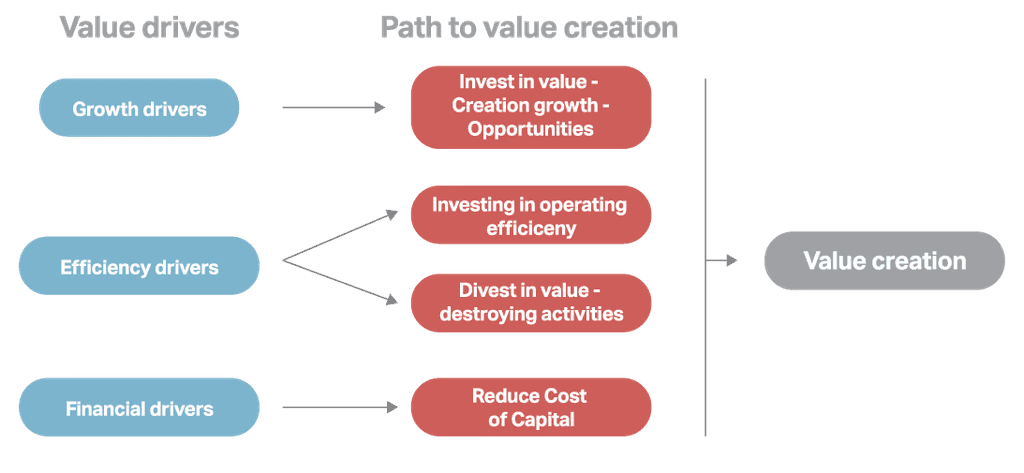

Key concepts

Advanced Financial Planning (AFP) – identify relevant value drivers, understand sensitivites and create what-if scenarios around key value drivers.

Value Based Management (VBM) as key concept to managing and executing strategy by identifying drivers that the company should focus on.

Measure and allocate cost of capital to optimize capital allocation

in an organization.When VBM and AFP are implemented, this can unleash tremendous value in the organizations by aligning strategy with operational execution and focusing the allocation of resources to where they can yield the highest returns.

Important read: White paper on Unified Performance Management

4.9 RATING

Trusted by finance and operation teams worldwide

with a 5-star rating and a Leader Badge on G2.

Advanced Financial Planning and Value Based Management

A white paper that outlines proper Advanced Financial Planning and Value Based Management through a practical example.

Key concepts

Advanced Financial Planning (AFP) – identify relevant value drivers, understand sensitivites and create what-if scenarios around key value drivers.

Value Based Management (VBM) as key concept to managing and executing strategy by identifying drivers that the company should focus on.

Measure and allocate cost of capital to optimize capital allocation

in an organization.When VBM and AFP are implemented, this can unleash tremendous value in the organizations by aligning strategy with operational execution and focusing the allocation of resources to where they can yield the highest returns.

Important read: White paper on Unified Performance Management

4.9 RATING

Trusted by finance and operation teams worldwide

with a 5-star rating and a Leader Badge on G2.

Advanced Financial Planning and Value Based Management

A white paper that outlines proper Advanced Financial Planning and Value Based Management through a practical example.

Key concepts

Advanced Financial Planning (AFP) – identify relevant value drivers, understand sensitivites and create what-if scenarios around key value drivers.

Value Based Management (VBM) as key concept to managing and executing strategy by identifying drivers that the company should focus on.

Measure and allocate cost of capital to optimize capital allocation

in an organization.When VBM and AFP are implemented, this can unleash tremendous value in the organizations by aligning strategy with operational execution and focusing the allocation of resources to where they can yield the highest returns.

Important read: White paper on Unified Performance Management

4.9 RATING

Trusted by finance and operation teams worldwide

with a 5-star rating and a Leader Badge on G2.